If you’re under contract, it’s tempting to treat insurance as a last-minute checkbox. But Arizona home insurance basics can directly affect whether you can close on time—and what you’ll pay if something goes wrong after move-in. Between monsoon storms, wind and hail, roof-age underwriting, and common exclusions (like flood), it’s worth slowing down long enough to make sure your policy matches the home you’re buying.

Below is a practical, buyer-friendly guide to homeowners insurance in Arizona: what it typically covers, what it often doesn’t, how deductibles really work, and what you should verify before you sign final closing papers.

Why home insurance can delay (or derail) closing

Your lender usually requires proof of homeowners insurance before they’ll fund the loan. That means you’ll need a policy lined up with:

- The correct property address

- The correct effective date (often the closing date)

- Adequate coverage limits (based on the lender’s requirements)

- A paid or confirmed first-year premium (depending on how your closing is structured)

If an insurer needs extra time—because the roof is older, the home is in a higher wildfire-risk area, or there are property features like a pool—your closing timeline can get tight fast.

This is one reason local guidance matters. A team like West USA Realty can help you anticipate what underwriters might flag based on the neighborhood, age of home, and typical construction in your area.

Arizona home insurance basics: what a standard policy usually covers

Most homeowners policies are built around a few main “buckets” of coverage. Understanding these buckets helps you compare quotes and avoid unpleasant surprises.

Dwelling coverage (Coverage A)

This is the amount used to rebuild the structure of your home if it’s damaged by a covered event (like a fire or windstorm). It’s not the same thing as purchase price or market value.

Arizona tip: Dwelling coverage should reflect rebuilding costs that can be influenced by labor availability, material pricing, and the home’s features (tile roof, custom finishes, masonry/stucco, etc.). Make sure your quote is based on accurate details—not rough guesses.

Other structures (Coverage B)

This covers structures not attached to the house, such as:

- A detached garage

- A storage shed

- Some fences or walls (coverage varies)

Personal property (Coverage C)

This covers your belongings—furniture, clothing, electronics—if they’re damaged or stolen (subject to policy limits and exclusions). Many policies set this as a percentage of dwelling coverage.

Smart move: If you have high-value items (jewelry, watches, collectibles, cameras), ask about scheduled personal property riders. Standard limits can be lower than people expect.

Loss of use / additional living expenses (Coverage D)

If a covered loss makes the home unlivable, this helps pay for temporary housing, meals, and related costs.

Liability coverage

This helps protect you if someone is injured on your property and you’re found legally responsible. It can also help with certain property damage you cause to others.

Arizona reality check: Pools, trampolines, and some dog breeds can trigger underwriting restrictions or higher premiums. If you’re buying a home with a pool, tell the insurer early—don’t assume it “doesn’t matter.”

The most common Arizona exclusions buyers misunderstand

Home insurance is full of “yes, but…” moments. These are some of the biggest ones buyers run into in Arizona.

Flood damage is typically not covered

A standard homeowners policy usually does not cover flooding. In Arizona, that matters because flash flooding can happen even far from rivers—especially during monsoon season.

If the home is in a flood zone (or if you simply want the extra protection), ask about flood insurance separately.

Earth movement is typically not covered

Damage from earth movement (earthquake, sinkhole, landslide) is often excluded or requires separate coverage. In many Arizona areas this isn’t a daily concern—but it’s still good to know it’s not “automatic.”

Wear and tear isn’t covered

Insurance is for sudden, accidental events—not gradual deterioration. An aging roof, old plumbing, or long-term leaks can fall outside coverage.

Deductibles: the number that matters when a claim happens

A deductible is what you pay out of pocket before insurance contributes.

You may have more than one deductible

Many Arizona policies include:

- A standard deductible for most claims

- A separate wind/hail deductible (sometimes)

- A percentage-based deductible for certain events (varies by carrier)

A low premium can look great until you realize the deductible is high (or percentage-based). Before you bind coverage, confirm:

- What the deductible is in dollars

- Whether any deductibles are percentage-based

- Whether wind/hail has a separate deductible

Roofs matter in Arizona (more than buyers expect)

Roof age and condition can change your insurance options quickly. Insurers may ask:

- How old is the roof?

- What material is it (tile, shingle, foam/flat)?

- Has it been repaired recently?

- Are there visible issues (curling shingles, missing tiles, ponding on flat roofs)?

Even if your inspection is clean, a carrier may still require documentation or limit coverage based on roof age. If you’re buying in areas with older housing stock—like parts of the Phoenix real estate market—starting your insurance shopping earlier can prevent last-minute stress.

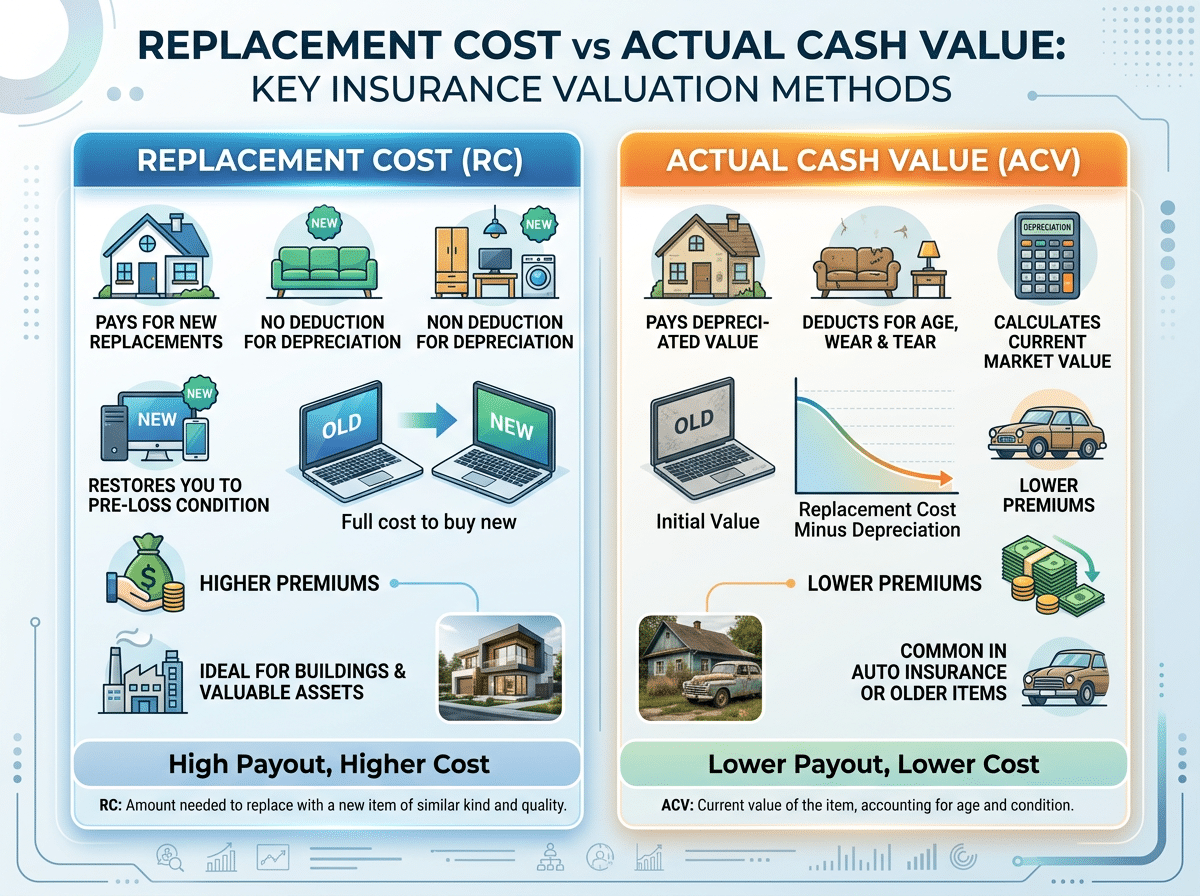

Replacement cost vs actual cash value: don’t gloss over this

This single detail can change the size of a payout dramatically.

Replacement cost (better protection)

Replacement cost coverage aims to pay what it costs to replace items (or rebuild) without subtracting depreciation—subject to your policy terms and limits.

Actual cash value (often cheaper, but riskier)

Actual cash value subtracts depreciation. If your roof, flooring, or belongings are older, the payout can be much less than the cost to replace.

Buyer takeaway: Ask whether the policy is replacement cost on the dwelling—and what the policy does for roof claims and personal property. “Yes, you’re covered” isn’t enough. You want to know how you’re covered.

Endorsements that are especially useful in Arizona

Endorsements are add-ons that fill coverage gaps. Not everyone needs all of these, but they’re worth asking about.

Water backup / sewer backup

This can help cover damage if water backs up into the home from drains or sewers (terms vary by carrier). In older areas or homes with certain plumbing setups, it can be a strong value.

Service line coverage

This can help with certain underground utility line repairs (again, terms vary). Surprise expenses here can be painful.

Ordinance or law coverage

If you have to rebuild after a covered loss, updated building codes may require changes. This endorsement can help cover those increased costs.

Extended replacement cost

Some carriers offer extra “buffer” coverage above your dwelling limit, which can help if rebuilding costs spike after widespread storm events.

Condo and townhome buyers: your insurance works differently

If you’re buying a condo or townhome, your HOA likely has a master policy. Your coverage needs depend on what the HOA covers (studs-out vs all-in varies by community).

- Condo buyers often need an HO-6 policy (interior + belongings + liability)

- Townhome buyers may need coverage closer to a single-family policy, depending on ownership and HOA responsibilities

If you’re still deciding between property types, you can compare options while browsing Arizona homes for sale and then confirm insurance expectations once you narrow the community.

What to have ready when you shop for quotes

Insurers can quote faster—and more accurately—when you provide clean details.

Have these ready:

- Year built

- Roof type and approximate age

- Square footage

- Construction type (block/stucco, frame, etc.)

- Any major updates (roof, HVAC, plumbing, electrical)

- Pool, spa, trampoline, or other liability features

- Prior claims history (if applicable)

If you’re buying in fast-growing areas like Queen Creek, it also helps to know whether the home is newer construction, because underwriting questions may be different than for older homes.

Closing logistics: what buyers should confirm with escrow and their lender

Before closing, confirm these items to avoid delays:

- The policy effective date matches your closing date

- Your lender is listed correctly as mortgagee (name/address must be right)

- You understand your escrow account setup (if your loan escrows insurance and taxes)

- You know how the first premium is being paid (at closing vs paid directly)

- You have the declaration page (proof of coverage) ready to send

If you want a broader view of timelines and “what happens next” after you go under contract, the Arizona home buying resources are a helpful refresher.

Quick “don’t close yet” checklist

Before you sign, make sure you can answer “yes” to these:

- ✅ My dwelling limit is based on rebuild cost, not purchase price

- ✅ I understand my deductible(s) in dollar terms

- ✅ I know what’s excluded (especially flood)

- ✅ I confirmed roof coverage details and roof-age requirements

- ✅ I added endorsements that match the home (water backup, service line, etc.)

- ✅ My lender has the correct proof of insurance

FAQs

How early should I shop for homeowners insurance when buying in Arizona?

As soon as you’re under contract (or even during the offer stage for unique homes). Roof age, pools, and prior claims can trigger extra underwriting steps.

Is flood insurance necessary in Arizona?

Not always, but flood damage is typically excluded from standard homeowners policies. Flash flooding during monsoon season can be a real risk depending on location and drainage.

Does my homeowners insurance cover roof replacement?

It depends on the cause of damage, your deductible, and whether the policy pays replacement cost or actual cash value for roof claims. Always confirm roof claim terms before binding coverage.

If I’m buying a condo, do I still need insurance?

Yes. The HOA master policy usually doesn’t cover everything inside your unit or your personal belongings. You typically need an HO-6 policy (details depend on the HOA policy).

What’s the biggest mistake buyers make with home insurance before closing?

Only comparing premium price. Deductibles, roof coverage, exclusions, and endorsements often matter more when a claim happens.

Final thoughts: protect your closing date and your future budget

Understanding Arizona home insurance basics is one of the easiest ways to avoid a stressful closing week—and one of the smartest ways to protect your finances after move-in. The goal isn’t to buy the “cheapest” policy; it’s to buy the policy that actually matches the home you’re buying and the risks you’re inheriting.

If you’re still shopping, start with homes that fit your lifestyle and budget by browsing Arizona homes for sale. And if you want a local expert to help you navigate the buying process—from offer to escrow to closing—connect with West USA Realty for guidance tailored to your Arizona neighborhood and timeline.